Advancements and Prospects of LNG Bunkering in the Australia-Asia Shipping Corridor

Progress and Developments in LNG Bunkering Infrastructure

The shipping industry serves as the backbone of global trade and the accessibility of reliable bunkering hubs is paramount for efficient operations. As we reflect on the developments of 2023, significant strides have been made in the LNG bunkering business within the Australia-Asia shipping corridor. This vital route, connecting the resource-rich landscapes of Australia to the busy markets of Asia, has seen a notable increase in the availability of LNG bunkering facilities. This growth emphasises a key shift towards sustainable fuel alternatives, driven by both regulatory pressures and industry initiatives.

Shipping lines traversing this corridor have been actively seeking new supply sources, diversifying their options beyond traditional hubs like Singapore and China. The emergence of LNG bunkering opportunities in the Pilbara region of Western Australia adds a new dimension to the landscape, offering a distributed and diverse supply network. This enhances the resilience of the bunkering infrastructure and fosters a more competitive market environment where ship owners can benefit from greater choice and flexibility.

LNG Bunker Fuel Market

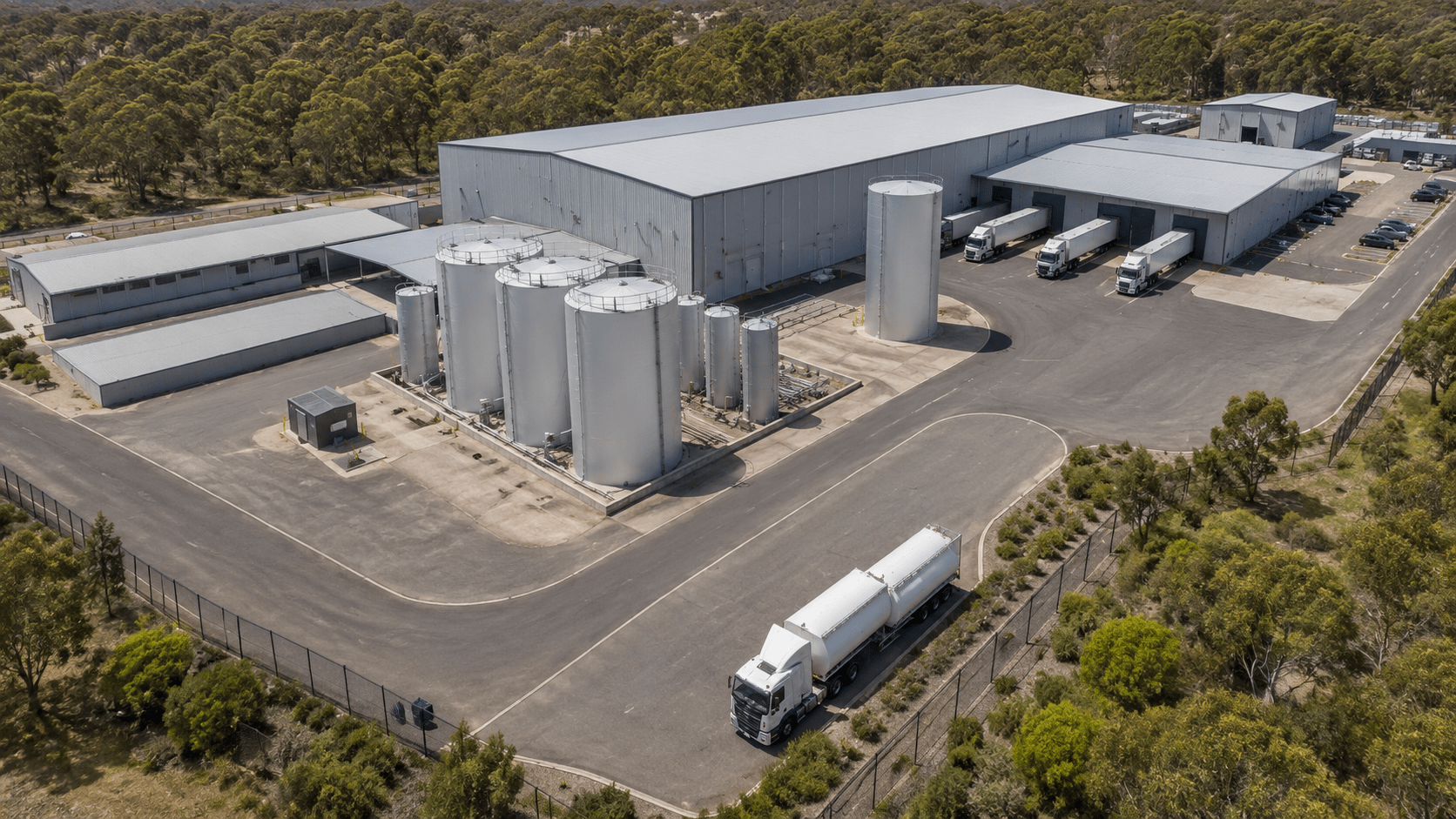

BE&R, based in Perth, Western Australia, has thoroughly analysed the LNG bunkering landscape in Port Hedland. The study aimed to collect industry data and forecast the growth of LNG bunker fuel demand in Port Hedland until 2040 without assessing the impact of LNG availability on demand growth. According to the study, the global adoption rate for LNG as a marine fuel currently stands at 47% of orders (as a percentage of gross tonnage). While interest in ammonia as a fuel is growing among bulk carrier ship owners and charterers, at-scale ammonia supply chains have yet to reach Final Investment Decision (FID). LNG remains the dominant alternative to low sulphur marine fuel oil and is witnessing significant demand growth.

A recent surge in LNG dual fuel orders by shipping companies servicing the Australia–Asia trade route has further increased the forecast LNG bunker demand. Currently, there are 70 vessels either operating or on order that are LNG dual fuel capable, with between 17 and 31 (Low to High case) likely destined to service the Port Hedland to Asia route. This translates to a potential demand of up to 0.5 MTPA by 2028.

Accounting for the increased efficiency of new ship designs, technology and operational practices, a potential opportunity of 20 to 40% reduction in fuel consumption and emissions is possible. However, this efficiency enhancement does not apply to the majority of existing tonnage, typically using 16,000 kW engines operating at a speed of 13.5 knots.

LNG Bunkering Vessel & Operations

Oceania’s LNG Bunker Vessel Specification

Oceania Marine Energy, a sister company of BE&R, has developed an LNG bunker vessel specification tailored to meet the requirements of the Port Hedland bunking operation. The bunker vessel is designed with simplicity in LNG handling, manoeuvrability, and environmentally friendly port operations in mind. Featuring reduced energy consumption and enhanced fuel efficiency, the vessel incorporates a hybrid energy supply comprising 2 x gas turbine generators and 2MWh battery packs for in-port operations. An essential aspect of the optimised design is the one-section mono-tank, along with modular machinery systems and subsystems, simplifying the building process for fast-track construction and low-cost operation and maintenance.

While Oceania’s base bunker vessel design is for a capacity of 6,000 m3, plans for expansion to meet growing demand include designs for 8,000 m3 and 12,500 m3 bunker vessels, maintaining alignment with the established design principles.

Competitive Analysis: LNG vs. Other Low Carbon Fuels

Amidst the increasing interest in low carbon fuels, LNG stands out as a frontrunner in the bunkering sector, thanks to its proven operational history and robust regulatory framework. One of the key metrics driving its adoption is its cost competitiveness, with LNG prices recently aligning closely with Very Low Sulphur Fuel Oil (VLSFO) on a $/MMBtu basis. This parity has been a significant driver for ship owners, incentivising them to invest in LNG dual-fuel tonnage. The steady growth in the LNG-powered bulk carrier fleet, with over 70 ships currently on the order book, attests to this trend.

In contrast, alternative fuels such as methanol and ammonia face considerable challenges, particularly in safety, supply chain scalability and price competitiveness. While technological advancements in ammonia engines and regulatory frameworks are underway, LNG maintains a distinct advantage in terms of market maturity and infrastructure development. However, collaborative efforts and regulatory support are ongoing and will be essential in addressing these challenges and fostering a level playing field for all low carbon fuel options.

Technological Innovations and Operational Strategies

Technological innovation lies at the heart of the LNG bunkering industry, driving efficiency gains and environmental sustainability. BE&R and Oceania’s development of LNG bunker vessel specifications tailored to the Port Hedland bunkering operation exemplifies this commitment to innovation. By incorporating hybrid energy supply systems and optimised vessel designs, Oceania aims to reduce energy consumption and enhance operational efficiency, while also ensuring environmentally friendly port operations.

Operational strategies such as bunkering during cargo loading and considerations for in-port bunkering highlight the industry’s focus on maximising efficiency and minimising downtime. These initiatives will streamline logistics and contribute to the reduction of emissions and environmental impact. As the industry continues to embrace technological advancements and operational best practices, LNG bunkering will undoubtedly emerge as a cornerstone of sustainable maritime transportation.

Ammonia Bunkering

Ammonia bunkering remains in the developmental stage and faces challenges similar to those faced by LNG in its early years, particularly in building supply chains alongside securing offtake contracts. Collaboration is increasing, notably with the establishment of Green Corridors between Singapore and Australia. Nonetheless, the price discrepancy and safety regulation remains a significant obstacle.

Sustainability leaders are urged to take the lead and invest in the entire value chain, spanning from production to bunker operation and ship delivery, to ensure readiness across the board. While initial pre-commercial demonstration pilot projects are underway, spearheaded by the Singapore Maritime & Port Authority (MPA) and Global Centre for Maritime Decarbonisation (GCMD), broader geographic efforts are needed to foster industry development along the green corridor. The Pilbara Port Authority is leading this effort in Australia’s Pilbara region.

Environmental Impact and Sustainability Initiatives

Beyond regulatory compliance, the LNG bunkering industry is increasingly focused on environmental impact and sustainability initiatives. The transition to LNG as a marine fuel represents a step towards reducing greenhouse gas emissions and mitigating climate change. However, achieving long-term sustainability goals will require a combined effort across the entire value chain, from production to bunkering operations.

Outlook for 2024: Opportunities and Challenges Ahead

The LNG bunkering business in the regions where operations have started, such as in Singapore have shown promising progress. The availability of LNG along the Australia to Asia shipping corridor is growing, with multiple shipping lines seeking new sources of supply. Collaboration efforts, such as the joint feasibility study with Oceania, Registro Italiano Navale (RINA), and Pilbara Clean Fuels (PCF) for the Port Hedland to Asia shipping route, indicate a commitment to further develop LNG bunkering infrastructure.

While challenges remain, the industry’s commitment to innovation, collaboration, and sustainability promises well for its continued growth and success. The LNG bunkering industry is ready to play a pivotal role in shaping the future of sustainable maritime transportation.